Most business owners spend years building their holding company, reinvesting profits, growing a portfolio, and watching value compound. Few pause to ask a fundamental question: what happens to that value when they die?

The Deemed Disposition at Death

When a Canadian resident dies, the Income Tax Act treats all capital property – including private company shares – as sold at fair market value, immediately before death. No actual transaction occurs, and no cash changes hands, yet the resulting capital gain is fully taxable on the deceased’s final tax return. For holding company shareholders with significant unrealized appreciation, this deemed disposition alone can result in a tax bill of hundreds of thousands, or even millions, of dollars.

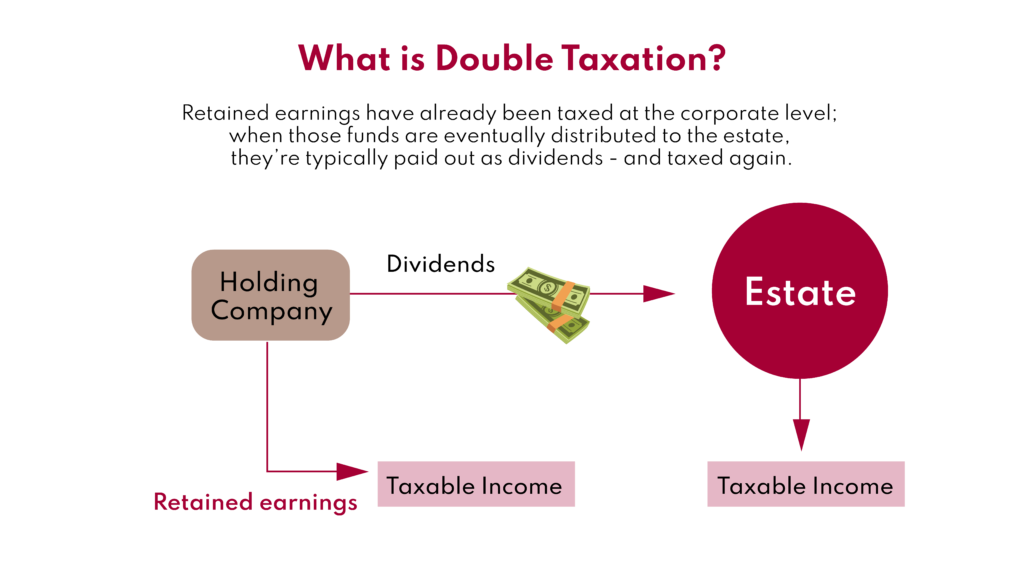

The Double Taxation Problem

The burden does not end there. Most holding companies hold investment portfolios that have already been taxed on the realized gains. When those funds are subsequently distributed to the estate or heirs, they are typically paid as dividends and taxed again at the personal level of the beneficiary.

This is what practitioners mean by double taxation on death: the same underlying corporate value is subject to capital gains tax on the deemed disposition within the holding company, and then the dividend paid is taxed again upon distribution. Depending on the province and the dividend character, the combined effective rate across these two layers can be much higher than initially expected.

The Spousal Rollover: Deferral, Not Resolution

If shares pass to a surviving spouse or a qualifying spousal trust, Canadian tax rules permit a tax-deferred transfer, postponing the capital gains tax that would otherwise arise on death. This rollover, however, does not eliminate the liability. It simply defers it until the second spouse’s death, at which point the holding company may have grown substantially, producing an even larger tax obligation.

The critical planning question is therefore: what steps should be taken between the first death and the second?

Post-Mortem Strategies

The Pipeline Strategy

A pipeline is a post-mortem corporate reorganization designed to extract value from the holding company without triggering a second layer of dividend tax. In simplified terms, the estate incorporates a new corporation (“Newco”), transfers the holding-company shares to Newco in exchange for a promissory note, amalgamates the two entities, and repays the note from the corporation’s assets. If structured correctly, only one layer of capital gains tax is payable.

Pipeline planning is well recognized by the CRA, which has ruled favourably on it in numerous technical interpretations. That said, it is highly technical, relies on administrative positions rather than specific statutory provisions, and must be executed with precision. Professional coordination shortly after death is essential.

The Loss Carryback

Under a loss carryback plan, the estate redeems shares from the corporation, triggering a deemed dividend but simultaneously creating a capital loss. That loss is carried back under subsection 164(6) of the Income Tax Act to offset the capital gain on the deceased’s terminal return, leaving the estate with one layer of tax at dividend rates rather than two, assuming losses are available.

The Lifetime Capital Gains Exemption

Where the shares held at death qualify as qualified small business corporation shares (QSBC shares), the Lifetime Capital Gains Exemption (LCGE) can shelter a substantial portion of the gain. The exemption limit was increased to $1,250,000 effective June 25, 2024, with indexation to inflation resuming in 2026.

Qualification requires that the corporation meet specific asset tests at the time of disposition and throughout the preceding 24 months. Holding companies that function primarily as passive investment vehicles may find these tests difficult to satisfy, but those with active business operations should review eligibility with a qualified tax advisor.

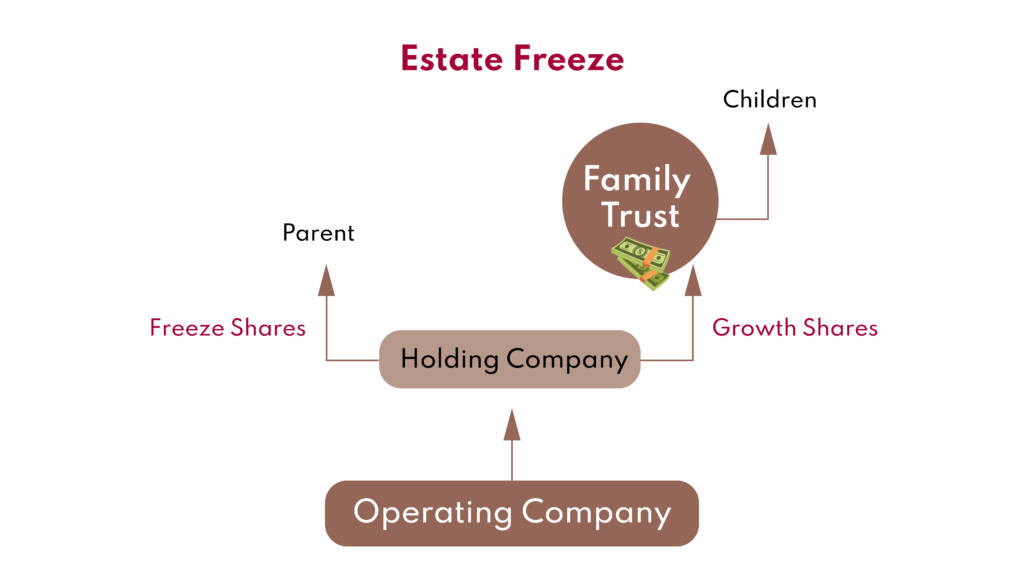

Lifetime Planning: The Estate Freeze

While post-mortem strategies address the tax consequences after death, the most effective planning occurs during the shareholder’s lifetime.

An estate freeze locks in the current value of a business owner’s interest, typically by exchanging common shares for fixed-value preferred shares, while directing all future growth to the next generation, often through a family trust. Because capital gains tax is calculated on appreciation, freezing the current value effectively caps the shareholder’s tax exposure at death and allows subsequent growth to accrue outside the estate.

Estate freezes are most effective when implemented early, while valuations are lower and planning flexibility is greatest. Waiting until a health event or an imminent sale constrains the available options considerably.

For holding-company shareholders, the essential takeaways are as follows. Death triggers a deemed disposition and an immediate tax liability. The spousal rollover provides a deferral, not a solution. Post-mortem strategies, the pipeline and the loss carry-back can prevent some or all double taxation but require timely, professional execution. An estate freeze, implemented proactively, can materially reduce the ultimate tax exposure. And corporate-owned life insurance can provide liquidity and tax-efficient funding to meet obligations when they arise.

If you have not reviewed your corporate estate plan recently, it is worth doing so while you still retain full control over the outcome. The most effective planning is deliberate, methodical, and well in advance of when you need it.