Saving isn’t glamorous. It means choosing to withhold spending now so you can enjoy more in the future, and let’s be honest: in your 30s, that’s anything but easy.

A growing career. A house, mortgage, and renovations. Kids, daycare, activities: In short, expenses grow faster than spring grass.

So here’s the big question: How do you know if you’re doing enough for your future?

Here are three financial goals to reach before turning 40.

Goal 1: Accumulate One Year’s Salary in Investments

The first goal is to build up the equivalent of one year’s gross salary in investments, excluding your home, bank account, and emergency fund.

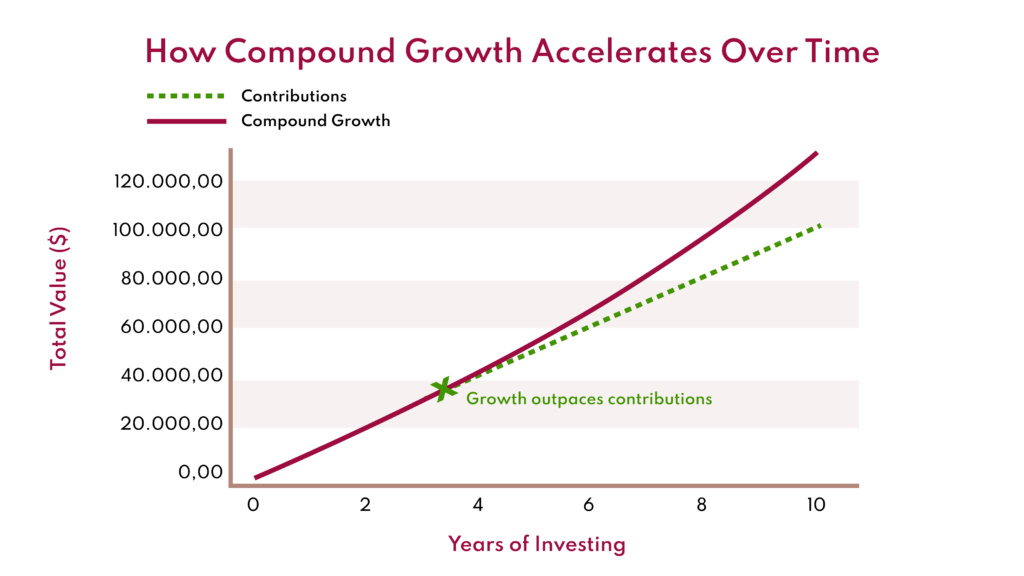

Why? Because it proves you’re living below your means. But more importantly, that’s when your savings truly start working for you.

Thanks to the magic of compound interest, your investments earn returns, which generate more returns, and over time, your savings snowball grows faster and faster with less and less effort. At some point, your annual returns will surpass your new contributions. In other words, it’s no longer you growing your portfolio — it’s your portfolio working while you sleep.

Goal 2: Maximize Your Tax-Sheltered Investments

The next step is to take advantage of the Canadian tax shelters available to you.

- TFSA: You can contribute up to $7,000 per year in 2025, and the contribution is cumulative since 2009, provided you haven’t maxed out your TFSA. All growth within a TFSA is tax-free, so you’ll want to try and max it out each year.

- RRSP: You can contribute up to 18% of your income per year, capped at around $32,000 in 2025. Contributions reduce your taxable income, and investments grow tax-deferred.

- RESP: If you have children, this is an ideal tool. You can contribute $2,500 per year, per child, and governments top it up—30% in Quebec or 20% elsewhere in Canada.

Governments don’t often hand out gifts. So when they do, please make the most of them.

Goal 3: Reach Three Times Your Salary in Investments by Age 40

Third goal: aim to have three times your annual income invested by 40. Ambitious? Yes. Achievable? Absolutely.

Is this realistic for someone who’s 30 and just starting to save?

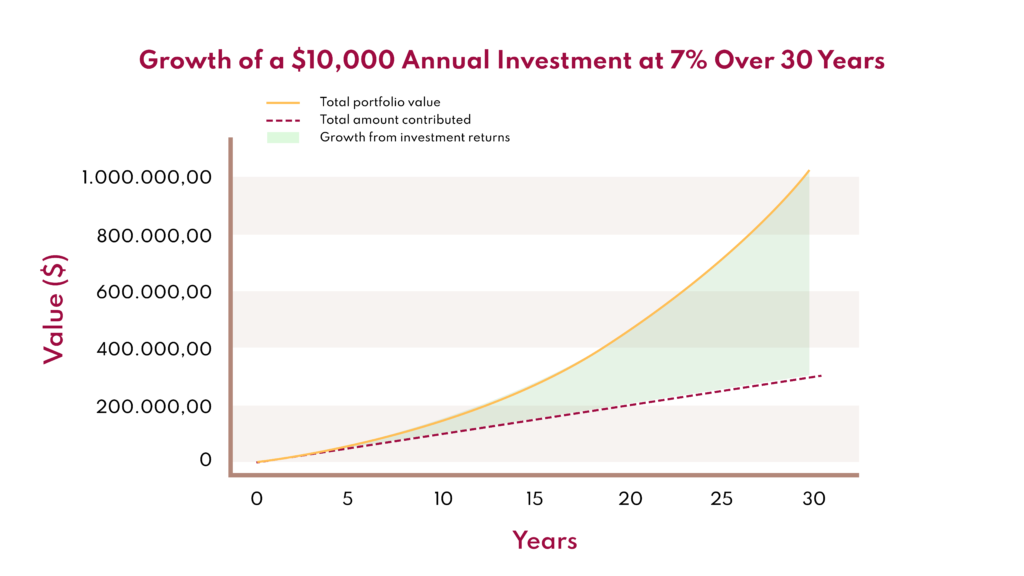

Let’s take an example. A 30-year-old earning $80,000 contributes 18%, or $ 14,400, to her RRSP and receives a tax refund of just over $5,000, which she uses to help fund her $7,000 TFSA contribution. She repeats this every year, earning 5% annual returns in both accounts for 10 years.

At age 40? She’d have $282,000 in savings—$42,000 more than three times her annual salary ($240,000).

The Real Secret: Time

Starting early isn’t a cliché — it’s leverage. Each year gained at the beginning of your journey adds thousands by the end.

Because one day, your investments will grow faster than you can save. And when that day comes, you’ll understand: time is your greatest asset.

In summary:

- One year’s salary invested;

- Maximize TFSA, RRSP, RESP;

- Three times your income in investments before 40.

And remember: these are general guidelines. Every situation is unique. What matters most is starting early, staying disciplined, and letting time work in your favour.