Are you a Canadian looking to buy your first home? The Tax-Free First Home Savings Account (FHSA) is a fantastic opportunity for first-time home buyers in Canada to save more money, tax-free, for their down payment.

FHSA Benefits: How it Works

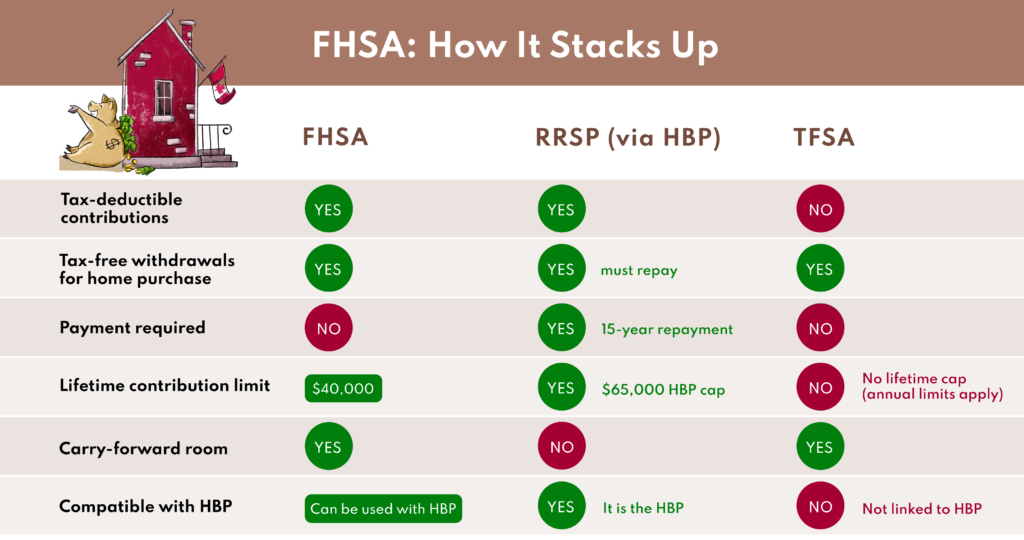

Some unique features to this investment vehicle make it different than existing accounts like the RRSP, TFSA or Home Buyer’s Plan (HBP). Here are some of the key benefits of the FHSA:

- Contributions to the FHSA are tax-deductible.

- Withdrawals from your FHSA to purchase a first home are also non-taxable.

- Returns on investments in your FHSA account are tax-free.

- You can make your down payment using funds from your FHSA and RRSP using your Home Buyer’s Plan (HBP).

- Unlike the HBP, funds don’t need to be repaid, and there is no withdrawal limit.

- You can contribute up to $8,000 a year, which can be carried forward if you don’t contribute the full amount (a maximum of $8,000 in contributions can be carried forward to the following year). Your contribution room starts accumulating as soon as you open your account, up to a lifetime $40,000 limit.

- If, after 15 years, you no longer plan to purchase a property, you can transfer the amounts to your RRSP without affecting your RRSP contribution room.

Who Qualifies for an FHSA

If you’re a resident of Canada between the ages of 18 and 71 and qualify as a “first-time home buyer,” and you or your spouse or common-law partner have not owned a home in the last four years, you may be eligible for the FHSA. Don’t forget to verify the other criteria to ensure you meet all the requirements.

But why should you consider the FHSA? Let’s face it, saving for a down payment in Canada can be tough. With the FHSA, you can contribute up to $8,000 a year, and the contribution room starts accumulating as soon as you open your account. This means you can start saving now and potentially have a handsome sum to contribute to your down payment in no time.

And let’s not forget that the HBP remains available to all FHSA owners, allowing them to withdraw up to $60,000 from their RRSP to buy their first home. If you meet the qualifications, you can make your down payment with funds from both your FHSA and RRSP using the HBP. This is a fantastic opportunity that lets you almost double your down payment. Plus, unlike the HBP, the funds withdrawn from your FHSA don’t need to be repaid, and there is no withdrawal limit.

Ready to take the first step towards homeownership? Open your FHSA today, as financial institutions are starting to open these accounts now, and start saving for your dream home. With tax-free savings, tax-deductible contributions, and nontaxable withdrawals, the FHSA is a fantastic investment vehicle that can help make your dream of homeownership a reality.

Don’t forget, after 15 years, if you no longer plan to purchase a property, you can transfer the amounts to your RRSP without affecting your RRSP contribution room. So even if your plans change, your savings don’t have to.

Start saving today and take the first step towards owning your own home.